Tough Times for Fintech

After 2 years of Covid-19 pandemic, just when we thought that the hard times were nearly over, reality hit us in February 2022 with the war in the heart of Europe. We don’t yet know what the long-term consequences of the global economic situation will look like, but we already see the impact in different areas of our lives and businesses in the EU. Many countries take care of refugees from Ukraine, support the attacked country with weapons and ammunition, impose sanctions against the aggressor and bear the consequences of these sanctions suffering under the high dependency on Russian gas and oil. The population is struck with high inflation and rapidly increasing prices. Many small businesses struggle to keep their heads above water due to growing energy costs. Startups in different areas experience venture capital funding curbs and shrinking valuation. And fintech is affected by these negative developments, too.

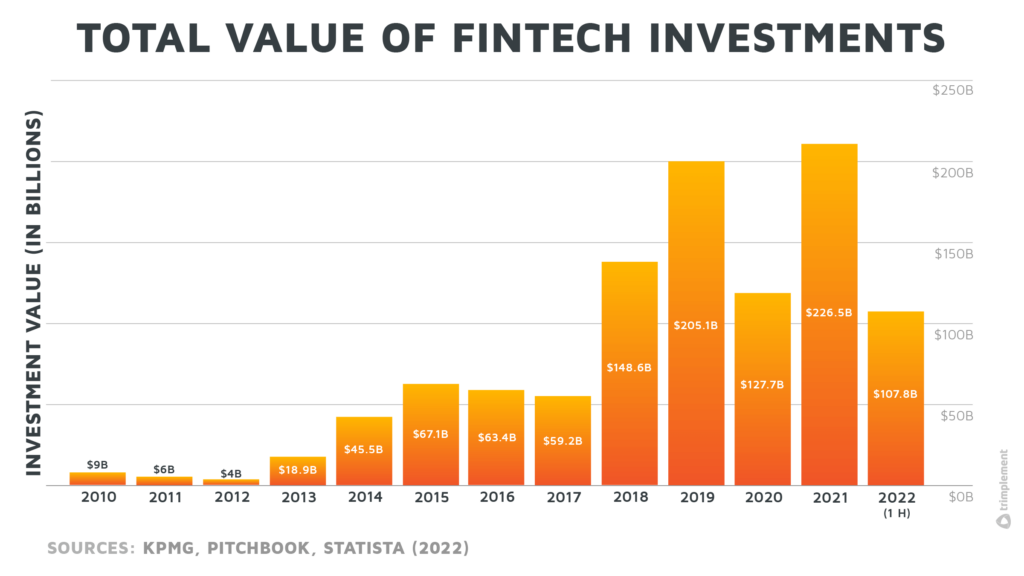

After the record year 2021, in 2022 the investments into fintech worldwide dropped from 226,5 billion USD to 107.8 billion USD. And it’s unlikely that the second half of the year will be as good as the first one. Most likely the deals that were closed in the first half of 2022 were negotiated at the end of 2021 / early beginning of 2022. That means, before the war in Europe and the recession started, under totally different circumstances.

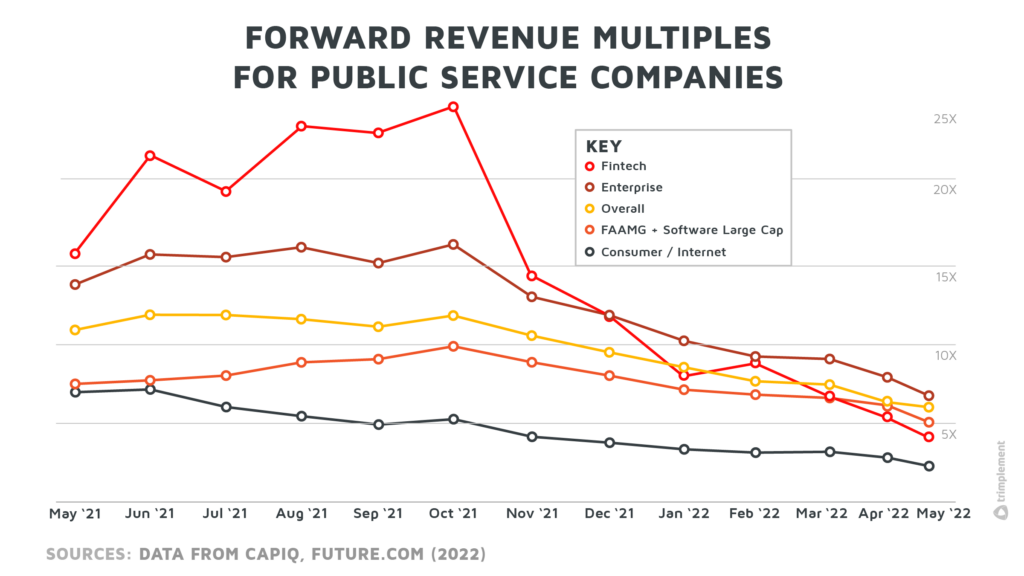

A report by Andreessen Horowitz shows that fintech companies valuations have fallen from 25 times forward revenue in October 2021 to four times forward revenue in May 2022.

But in times of trouble there is also always a place for business success and some use cases that become relevant thanks to the crisis – even if it sounds strange at first glance.

Today I would like to talk about fintech in a time of crisis and check what type of products could be the winners in the current political and economic situation.

Refugee Wallet and Welfare Management

When refugees are coming into a new country they are typically frightened, traumatized, physically and mentally exhausted. Often they don’t speak the local language. And then they are overwhelmed with all the bureaucratic requirements, rules that they need to comply with and forms that they need to fill in to get the needed support and benefits of the state. So very often, especially in big cities, the processing of application documents takes months. In the best case, the refugees find a local family which helps them to orient themselves in this challenging situation, but not everyone is so lucky to find one.

On the other hand, the state institutions responsible for the refugees may also be overwhelmed by a big number of refugees coming into a city at once. Many processes are still executed offline and combined with a lot of paperwork. Sometimes there is also a problem of understaffing. So any kind of simplification and digitalization of the refugee reception and support distribution (whether in form of goods or money) would be a big benefit for both sides.

When we think about the fintech area, we believe that some kind of a refugee welfare management platform would be helpful. It could be a digital e-wallet combined with an administration system for state employees. Every registered refugee would automatically get an account (a wallet) in this system without the need to open a real bank account. The corresponding state institutions could transfer money or other digital assets to those wallets (e.g. points that can be spent in certain dedicated shops only). The refugees in turn could use a mobile application on their smartphones or prepaid cards which are bound to their refugee wallets to be able to pay for services and goods. If the state is giving support in the form of goods, the distribution of those goods could also be tracked in the system which provides transparency to all participants. In addition, if the laws of the country prescribe limitations with regards to the type of goods and services on which the refugees are allowed to spend their subsidy (e.g. no alcohol), this could be implemented accordingly in the mentioned management solution.

The refugee welfare management platform could also contain further features. For example, for those who rent out apartments to the refugees. These landlords could also get a special landlord wallet on the platform and receive their rental fee there with the possibility to withdraw their money to a bank account or alternatively to have also a debit card which is bound to their wallet.

Charity Donations / Crowdfunding

Another fintech solution of relevance would be a platform allowing a private person or a company to easily collect money from different people or companies and spend it on different charity goals: for example on equipment for the army, support for refugees, for injured people or orphaned children or any kind of donation projects you can think of.

Such a platform should allow the registration of a funds collection project with a financial account (it may be a full-blown bank account or just a digital wallet) by a private person, an NGO or a business company. Of course, proper verification flows have to be supported to avoid any fraud and scam.

Ideally, this financial account/wallet should be able to receive any kind of fiat or crypto money donations and convert them to the target currencies as people all over the world may want to help. Also, it should support as many payment methods as possible allowing donors to pay by their preferred currency and method.

According to the country of residence of the account owner, certain rules and regulations may apply so that the platform has to be flexible and adaptable to local laws.

The most challenging part is the implementation of spending of the collected money. It should be made transparent to every donor who has sent some money to support a certain charity action. And then there are special challenges. Sending money to a certain person in an authoritarian country via standard payment methods like bank-to-bank transfer may be impossible, because the country may prohibit receiving funds from abroad. So another channel of payment may be needed.

The platform should also ideally be able to promote different charity campaigns on relevant websites and on social media. This is the minimum amount of features that such a platform should have from my point of view. Further analysis may discover other useful functionalities not mentioned here.

Of course, there already are solutions allowing the collection of money for charity goals. Even PayPal and the Facebook platform allow you to execute small donation projects. However, those solutions often are limited in their functionality and don’t provide support for non-standard payment methods, currency conversion or spending transparency.

Smart KYC and AML Solutions

During the months after February 2022 the US, the EU, the UK and other countries have sanctioned more than 1,000 Russian individuals and businesses – including so-called oligarchs. These are wealthy business leaders who are thought to be close to the Kremlin and Putin, such as former Chelsea FC owner Roman Abramovich. Due to the mentioned sanctions against Russian businessmen, sophisticated know-your-customer and anti-money-laundering solutions would be needed to monitor the financial activities of sanctioned persons and persons that are related to them.

Those KYC and AML solutions should ensure that the sanctioned persons don’t find any back doors to execute financial transactions either stealing the identity of other people or letting other people do financial transactions on their behalf. One famous example of such prohibited financial actions would be Russian billionaire Oleg Deripaska’s sanction violation: “The U.S. Department of Justice said Deripaska violated sanctions by using the U.S. financial system to maintain three luxury properties and employing a woman to buy a California music studio on his behalf.” The KYC and AML checks in a financial institution should be smart enough to discover such kinds of relationships and activities and raise the alarm in the system.

Of course, there are definitely more fintech use cases that become relevant in times of crisis. Many of them can be built using our software framework Finergizer – a platform for building innovative custom-tailored payment solutions. Reach out to us if you have an idea and are looking for experts that could help you to create a fintech product based on your concept.