Hypes are a good thing. No, think about it: They generate attention for products, activities and ideas. And where there is attention, there is scrutiny, too. The humming of the mainstream buzz makes us turn heads and observe closely where the noise is coming from.

For the hype-sensitive stock market, this has proven a boon in many cases. Wall Street is loud, and the more volume an investment trend generates, the more it will catch regulators’ interest – besides that of eager venturers. And currently, one investment trend generating much noise is that of SPACs.

SPACs (short for Special Purpose Acquisition Companies) stood on the sidelines of the stock markets for a few decades. But in recent years, they made a comeback in the investment mainstream – mostly thanks to the web. And there, I could not help but think of another social-media-driven hype of the 2010s: ICOs.

In fact, SPACs already show the same signs of overvaluation and ultimately disintegration that have befallen ICOs a few years back. But will SPACs go down the path of the ICO?

In this article I will try to answer this question and a few more, like:

- What are SPACs?

- Why are they popular?

- What are their risks and disadvantages?

- Is the SPAC hype comparable to the ICO hype?

Okay then, here goes: SPACs, the specifics…

What Are SPACs – A Definition

A Special Purpose Acquisition Company (or SPAC) is a blank slate company listed on a stock exchange. Its objective is to acquire or merge with other private companies to bring them public without the need for a conventional initial public offering (IPO) on their side.

To reach that goal, a SPAC’s venture undertakes several steps, most quite similar to IPOs. Most of the actions below take place within a 2-3 year timeframe. After the launching period taking around 8 weeks, the SPAC faces a liquidation window of 24 months at most. If the acquisition company doesn’t find a suitable merging partner, investments gathered so far return to the shareholders. Many SPACs prolong this period by signing agreements or letters of intent before it runs out or literally “buy time” by injecting additional funds into the SPAC trust.

The Process of Pushing a Company to the Stock Exchange via SPACs

1. Forming and Launching the SPAC

It all starts with founding the Special Purpose Acquisition Company in question. The people launching such a company go by the term Sponsors. Sponsors promote their SPACs, conduct market research for the respective industry and tow potential investors and acquisition targets.

2. Bringing in Institutional Investors

After the SPACs foundation, sponsors raise money on a typical IPO roadshow – including one-on-one meetings with potential institutional investors. Special Purpose Acquisition Companies don’t have an actual product or business idea in the pipeline. Instead, they try to win institutional investors over by emphasizing “softer” factors: the SPAC’s team experience and composition, domain knowledge.

For investors though, buying into a SPAC is still a leap of faith. At this point, the blank check company can not yet tell the shareholders-to-be which enterprise they want to acquire or which industry to target.

However, institutional investors can look forward to favorable conditions: In addition to their share of common stock, they receive warrants or fractions thereof. Those warrants allow them to buy more stocks of the “combined” company at a fixed rate.

3. Maintaining a Trust

The money moves into a blind trust and stays there until the SPAC announces the company-to-acquire and the shareholders approve. Typically, the SPAC team uses around 2% of the investments, plus an additional $2 million to pay the filing and legal costs, ensure due diligence and maintain operations of the SPAC.

Aside from that, the funds remain untouched. That means, the stock price remains stable in this phase: One SPAC share usually costs $10 – mostly out of tradition, but the low price tag also helps drawing in small-time investors. After the acquisition, this price will be determined by the stock market.

4. SPACs Going Public

With the initial investment finished, the SPAC goes public at a stock exchange. Now retail investors may obtain shares at a fixed price as well. Some SPAC teams decide to disclose information on the industry they target in the coming acquisition, hoping to draw in more prospects.

Note that retail investors don’t benefit from the same purchase conditions as institutional investors, receiving no warrants for example.

5. The Investors’ Vote

During the above phases, SPAC sponsors have been on the lookout for fitting target companies. But at some point, before the liquidation window expires, they inform their institutional investors about the company or companies they have chosen for acquisition – but only after the SEC or a similar institution has reviewed the deal. This can take up to 4 months again. When that’s done, investors receive a so-called proxy statement containing information about the company-to-acquire. Afterwards, the investors vote, deciding whether they want the merger with or acquisition of one of the chosen companies to occur or not.

A few years back, the choice of “yes” or “no” was attached to either keeping their funds in or pulling them out. This led to messy situations for SPACs. Sometimes investors threatened to sabotage the deal if they didn’t get preferential treatment. New regulations have solved this problem by untying the right to vote from the right to bail out. Investors can now withdraw their funds, even if they vote “yes”. They no longer have the pressure to reject the deal altogether if they change their mind about their investments.

6. De-SPAC Phase

This is the phase when the actual acquisition happens. The “blank slate” is filled with another company through a so-called “business combination” (i.e. a merger or an acquisition). Doing so, the SPAC takes the said company public. The name on the stock market ticker is adjusted to reflect that change. Stocks of the acquired company can now be traded and are subject to the ups and downs of the market.

Note that even well-performing SPACs might not have raised enough money initially to cover the whole expenses of the planned acquisition. SPACs often pick out target companies multiple times their size and value. In addition, they don’t announce the target to retail investors before the De-SPAC happened. Thus, acquisition companies cannot hope to draw in more investors by choice of target. Yet there are ways for SPACs to bring in additional money. Public equity (“PIPE”) deals or committed debt with private investors are common practices here.

The SPACs Hype – Then and Now

Blank slate mergers for easy stock market listing first came up decades ago. In the 70s, the concept of Reverse Mergers (also called “Reverse Takeovers” or RTOs) established itself. There, successful companies merged with company shells or non-operational, but public firms, to quickly get their own shares out in the market. The practice had a bad record: From the 1990s to the 2010s Reverse Takeovers were notorious for being quick access points for foreign investors to the American stock market.

SPACs evolved out of Reverse Mergers. And they inherited their bad reputation. SPACs are more obtrusive than RTOs, as their sponsors are proactively searching for acquisition/merging partners – including risky ones.

Appropriately enough, SPACs have shown much presence in the headlines of financial papers recently. In 2017, Entrepreneur Chamath Palihaptitiya laid the foundation stone for the SPACs hype. He raised $600 million for the SPAC Capital Hedosophia Holdings and acquired a 49% stake in the spaceflight company Virgin Galactic. And there are other examples of successful SPACs: Did you know that Burger King went public again in 2012, basically using the SPAC method?

Nowadays, many venture capitalists and privately investing celebrities like rapper Jay-Z or soccer player Robert Lewandowski involve themselves in SPAC ventures – and increase their mainstream appeal through social media cheerleading. This generated a run on SPAC shares by retail investors. Still, the curve points upward: A few months into 2021, SPACs have garnered more than US$ 97 billion, which already surpasses the US$ 83 billion mark set by 2020.

Why Are SPACs So Popular?

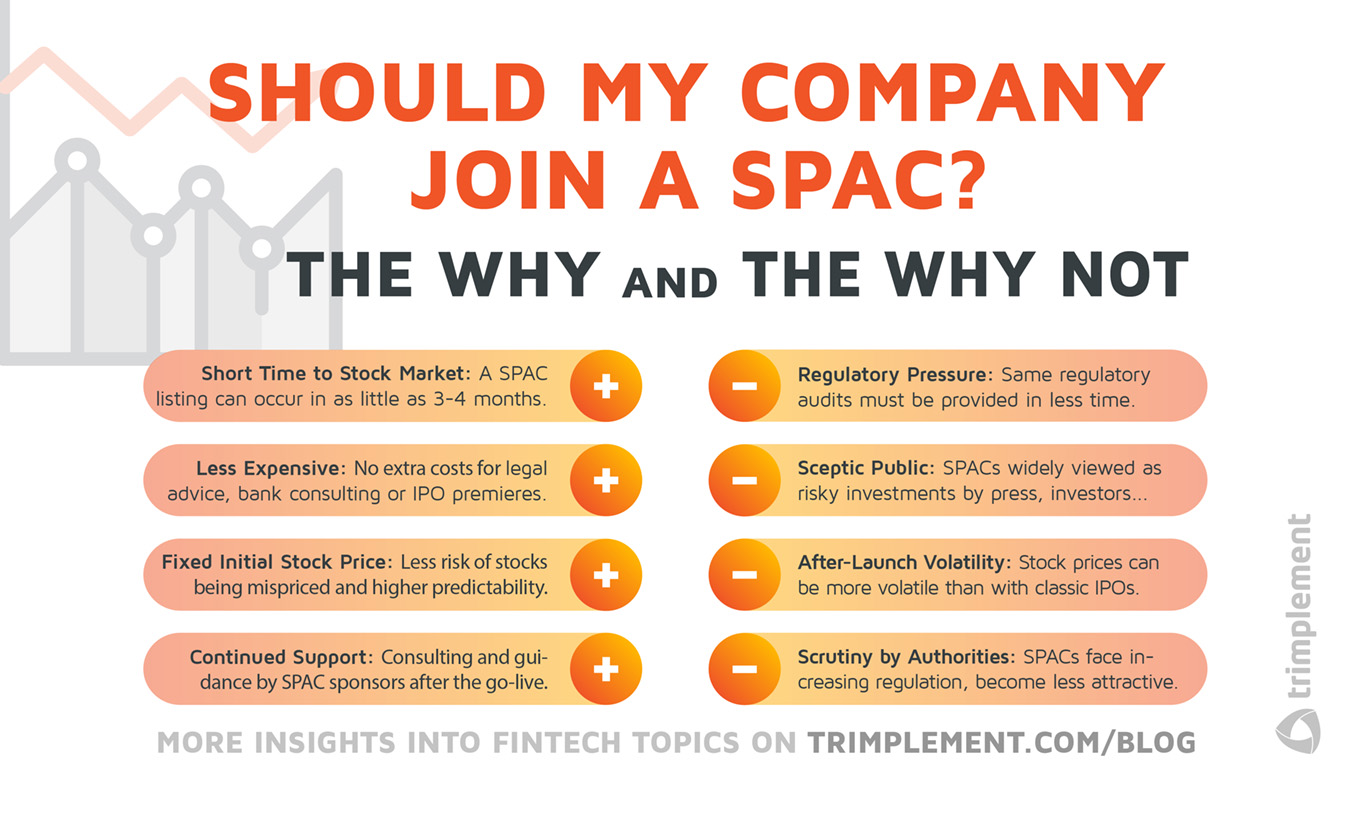

But SPACs are not only popular with private investors: For companies that want to skip a few steps on the climb to the stock market, SPACs promise a viable shortcut. A SPAC-propelled listing can happen within a timeframe of only 3-4 months. Now compare that to the 2-3 years a traditional IPO would require!

Especially now this comes in useful. Many companies who wanted to go public and raised capital were stopped cold by the COVID-19 pandemic – just as many other aspects of finance and commerce were. Merging with a high-profile SPAC, they can execute their plan with less friction.

What’s more, merging with a SPAC often also saves efforts for legal advice and investment banking consulting – let alone expensive stock market premieres. At the same time, companies have higher security about the initial value of their stocks. In regular IPOs, the share’s price is dependent on the market situation. This can play out in favor of companies if their shares are in high demand. Yet, IPO bankers can also put a misguided price tag on their shares, leaving them with less, than they expected. In comparison, SPAC stocks are more predictable, being initially sold at fixed prices – a company knows exactly what their stocks and their company is worth exactly upon launch.

That said, a company merging with a SPAC is not exempt from regulation altogether. Before the merger happens, the SEC or similar authorities will become active. Target companies then have to provide customary attestations of due diligence, tax documents, internal audits, etc. And they have to do this in a timeframe of a few months, which is much shorter than that for regular IPOs.

SPACs vs. ICOs?

The SPAC boom is not the first investment phenomenon stoked by lofty promises. It shows parallels to another hype: The hype around ICOs. ICOs or Initial Coin Offerings describe the practice of start-up companies to create a crypto token traded on the blockchain. Private investors can buy it as part of an initial offering, as a means to provide funds to the startup. The promise: With the company’s rise in value, the crypto token will also become more valuable and can be sold again for a profit or be used to pay for goods and values.

In the vast majority of cases, ICOs did not keep that promise. But some did: Ethereum, in many ways the prototypical ICO, is perhaps the most well-known success story in ICOs. Regarding cryptocurrency market cap, its second to Bitcoin only. Yet, many other ICO companies disappeared as quickly as they manifested and many venturesome investors lost their funds. In a significant number of cases, ICOs used the fact that blockchain-based projects in the crowdfunding and crowd investing area were unregulated to commit fraud: Shady companies promoted ICOs without even having a business plan and cashed in on investor’s fear of missing out.

The vulnerability to fraud and investment loss eventually caused the ICO hype to die down. That does not imply that they were not successful during their prime: Between 2014 and 2019, ICOs raised a total of $26.17 billion. And as an instrument, ICOs are still in use albeit in much smaller numbers than during the high times.

The Similarities of SPACs and ICOs

Now, there are crucial differences between SPACs and ICOs. The former operate on a highly regulated market. The latter do so on a largely unregulated one, due to the decentralized nature of the distributed ledger technology behind them. But SPACs and ICOs still have common elements, mostly in their more negative aspects:

- Alternatives to IPOs: Both form an alternative to classical IPO fundraising, for investors as well as companies. Of course, ICOs lack the prestige that comes with being listed on a stock market.

- Risk of Poor Deals: Both are susceptible to lead investors to support companies of low quality. In the case of ICOs, companies in bad faith and without the hint of a business plan used their Coin Offerings to gather funds from unwary investors. With SPACs, it’s at least possible that unsustainable companies are brought live. When the end of the liquidation window approaches, investors get nervous and high-profile companies have already put sponsors off, the willingness to acquire less than ideal targets might rise. At least if sponsors – typically owning around 20% of their own SPACs shares – don’t want to lose the investment they brought in up to that point.

- Little Investor Security: Actually, SPACs are a relatively safe bet for institutional investors, due to their specific conditions: If they don’t like what they see, they can withdraw their money. ICOs might offer the same, granting privileges to special investors. Retail investors are out of luck though, in both cases. With ICOs back then and with SPACs now, they are obtaining the proverbial pig in a poke. They purchase shares of an unknown company they can only hope to be profitable one day. In most cases, this doesn’t work out: On average post-acquisition SPAC stocks lose 12% of their value during the first year.

- Regulatory Scrutiny: Both are nervously eyed by regulatory authorities. More about that in a moment.

Will SPACs Meet the Same Fate As ICOs

One key aspect, that caused the hype around Initial Coin Offerings to fade, was increasing scepticism. There are varied ways of misusing ICOs for fraudulent ends. Many of them made headlines, and the whole ICO investment practice gained the reputation of being prone to fraud and pure speculation. Ultimately, they fell from grace as an investment method, on the grounds of a number of dubious players.

In many regards, SPACs are embarking on the same path. Investment experts and stock market analysts increasingly doubt the sustainability of the SPAC investment model. With a lack of high-profile companies that want to avoid bad press, many sponsors are already struggling to find suitable acquisition targets. They then join with immature firms. Most of these have sometimes business strategies as thin as the notorious ICO companies in the heydays of crypto coin speculation.

This leads to worse deals, which puts off even more potential investors and companies. And the ones who still get involved might feel defrauded by low returns, asking for more regulation. In the end, SPACs will face a shriveled pool of target companies. Most of those will be immature and don’t counterbalance the investments.

And this causes the SPAC bubble to finally burst.

What Will the Future Hold for SPACs

Of course, we can only speculate whether this scenario will befall Special Purpose Acquisition Companies. Yet, the current dynamics around SPACs are hard to ignore. SEC Chairman Jay Clayton told Havard Business Review that SPACs will be held accountable to the same rigid disclosure practices as IPOs, hinting at stricter regulations. For example, some experts argue, that the very idea of “blank check” companies could violate the disclosure requirements of stock markets.

Moreover, while SPACs saw tremendous growth in the US, they don’t take root on the European stock markets: 10 SPAC listings in the EU stand against 522 listings in the US. The discrepancy likely results from the tendency of European companies to go public after having reached higher maturity than their US counterparts.

But maybe, SPACs are just a staging post towards an entirely new form of investments – one more secure for investors. ICOs, again, provide an example here: Regulators, naturally wary of decentralized systems, did not hesitate long to undertake the first steps towards cryptocurrency regulation. Today, ICOs still exist, but without the huge hype factor. On the same note, new forms of crypto investments have evolved out of ICOs, such as the more regulated STOs and IEOs.

In my opinion, SPACs might not exactly serve as a shellproof financial investment. But certainly, it will be worth keeping an eye on what might evolve from them.